From Penny Pinchers to Credit Addicts: America's Complete Financial Personality Transplant

Your great-grandmother probably saved her money in coffee cans, mason jars, or literally under her mattress. She paid cash for everything, saved for months before making any purchase, and would have been mortified by the idea of borrowing money for anything except a house. Today, the average American carries $6,194 in credit card debt and thinks nothing of financing everything from groceries to vacations.

This isn't just a change in financial tools—it's a complete rewiring of the American relationship with money that happened in less than a century.

When Debt Was a Dirty Word

For most of American history, owing money was considered a moral failing. Families would go without rather than borrow, and being in debt carried genuine social shame. The phrase "neither a borrower nor a lender be" wasn't just Shakespeare—it was a core American value.

Photo: Shakespeare, via cinehunden.com

Photo: Shakespeare, via cinehunden.com

In the 1920s, the average American household saved 15% of their income. Not because they were planning for retirement or college funds, but because that's simply what responsible people did. You saved until you could afford what you wanted, and if you couldn't afford it, you didn't buy it.

This mentality created some behaviors that seem almost alien today. Families would save for years to buy a refrigerator or a car. They'd repair clothes until they literally fell apart rather than buy new ones. The idea of buying something you couldn't afford was as foreign as eating food you couldn't digest.

The Cash-Only Culture

Before credit cards existed, American commerce ran entirely on cash and checks. This created natural spending limits that forced people to think carefully about every purchase. You couldn't spend money you didn't have because you literally didn't have access to it.

Grocery shopping meant counting out bills and coins at the checkout. Buying a car meant showing up at the dealership with an envelope full of cash or a certified check. Vacations were planned months in advance because families needed time to save the actual money they'd spend.

This cash-based system also made spending much more psychologically difficult. Handing over physical money creates a psychological "pain of payment" that swiping a card doesn't trigger. Every purchase required a conscious decision to part with something tangible.

The Great Savings Culture

American families didn't just save money—they built entire cultural rituals around it. Children received piggy banks as soon as they could hold them. Families had "rainy day funds" that were considered as essential as having food in the pantry. The concept of "making do" wasn't about being cheap—it was about being responsible.

Women often managed household finances through elaborate cash envelope systems, allocating specific amounts for groceries, utilities, and discretionary spending. When the envelope was empty, spending stopped until the next payday. This created natural budgeting that required no apps, spreadsheets, or financial advisors.

Bank savings accounts were treated almost like religious institutions. Families would make weekly deposits, no matter how small, and watched their balances grow with genuine pride. The passbook showing your accumulated savings was a symbol of financial virtue.

When Everything Changed

The transformation began in the 1950s with the introduction of the first credit cards, but it accelerated dramatically in the 1970s and 1980s. Banking deregulation allowed credit card companies to charge higher interest rates and target customers more aggressively. Suddenly, Americans were receiving pre-approved credit offers in their mailboxes.

The cultural messaging around debt began shifting from shame to empowerment. Credit cards were marketed as financial tools that provided "flexibility" and "convenience." The stigma around borrowing money gradually disappeared, replaced by the idea that credit was a smart financial strategy.

By the 1990s, carrying a credit card balance became normalized. The phrase "good debt" entered the American vocabulary. People began talking about "leveraging credit" and "building credit history" as if these were sophisticated financial strategies rather than simply owing money.

The Numbers Tell the Story

The statistical transformation is staggering. In 1960, American households saved an average of 13% of their income. By 2005, the savings rate had dropped to just 2.6%. Meanwhile, household debt as a percentage of income skyrocketed from 60% in 1980 to over 130% by 2007.

Credit card ownership went from virtually zero in 1960 to 83% of American adults by 2020. The average American now has 3.84 credit cards and access to over $30,000 in available credit. What was once an emergency financial tool became the primary way Americans manage their daily expenses.

The Psychology of Plastic

Credit cards didn't just change how Americans spent money—they changed how we think about money. The psychological distance between swiping a card and parting with actual money made spending feel almost abstract. Studies show people spend 12-18% more when using cards instead of cash, simply because the transaction feels less real.

The "buy now, pay later" mentality extended beyond just purchases. Americans began thinking about future income as current spending power. The idea that you could enjoy something today and worry about paying for it later became not just acceptable but financially savvy.

Living Paycheck to Paycheck in the Credit Age

Despite having access to more credit than any generation in history, 63% of Americans can't afford a $500 emergency expense. This represents a complete reversal from the cash-based era, when families specifically saved for unexpected expenses.

Modern Americans often have higher incomes than their grandparents but feel more financially stressed. The constant access to credit creates the illusion of financial flexibility while actually increasing financial fragility. Easy borrowing replaced the financial discipline that cash-only living naturally imposed.

What We Gained and Lost

The credit revolution gave Americans unprecedented access to goods, services, and opportunities. Families can buy homes earlier, students can invest in education, and entrepreneurs can start businesses without waiting years to accumulate capital.

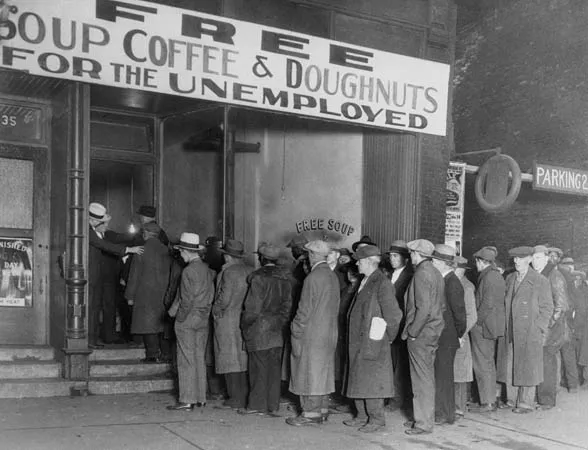

But we also lost the financial resilience that came from living within our means. The generation that survived the Great Depression understood money in ways that seem almost foreign today—they knew the difference between wanting something and needing it, and they had the patience to save for what they wanted.

Photo: Great Depression, via hoovervillet.weebly.com

Photo: Great Depression, via hoovervillet.weebly.com

The next time you swipe a credit card without thinking twice, remember: you're participating in a financial behavior that would have horrified your great-grandparents. Whether that's progress or decline depends on how you look at it—but there's no denying it's a complete transformation of what it means to be financially American.